Why Did My Insurance Premium Go Up?

If you’ve opened your renewal notice recently and noticed your insurance premium increased, you’re not alone. One of the most common questions insurance professionals hear today is, “Why did my insurance go up when I haven’t filed a claim?”

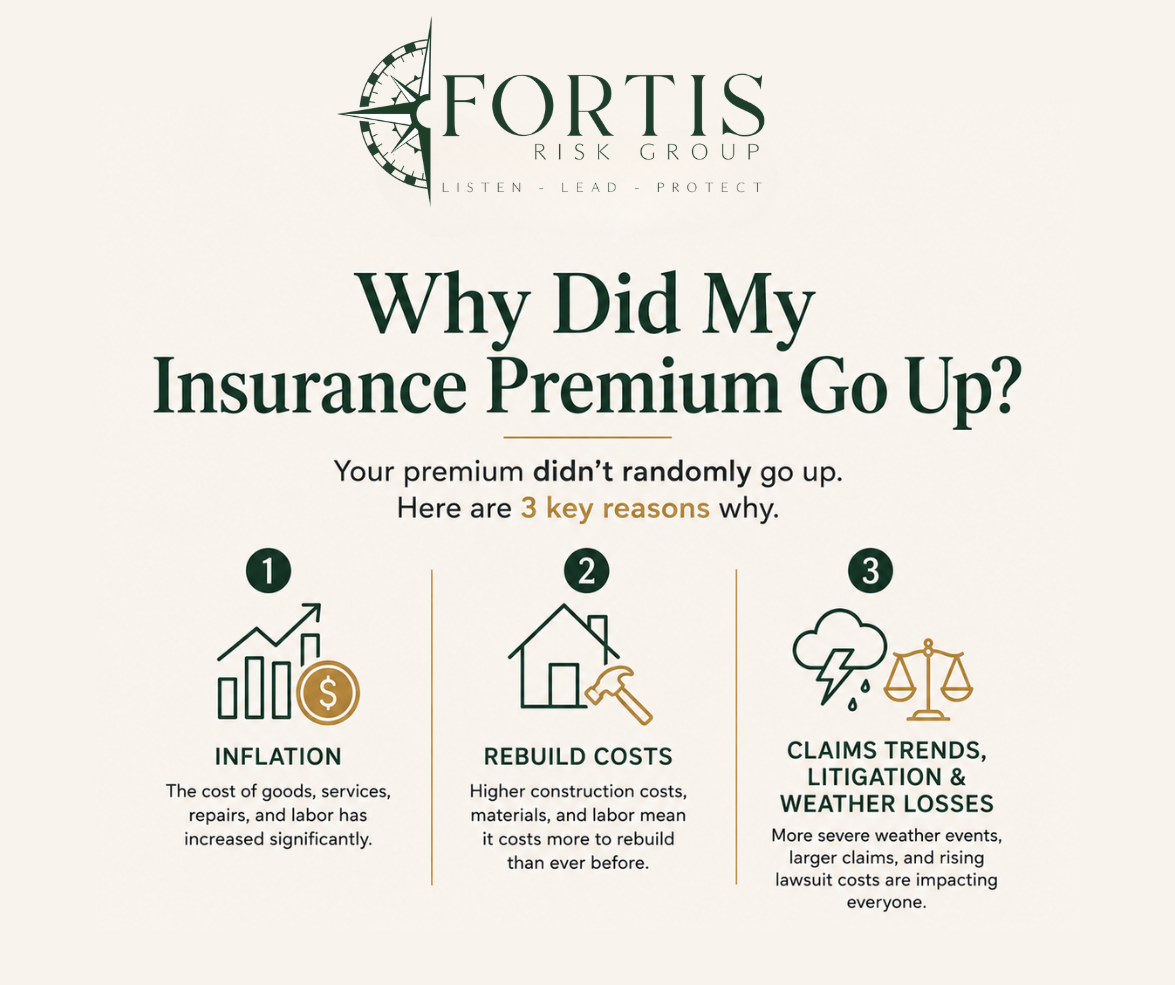

The reality is that your premium didn’t randomly increase. Insurance pricing is influenced by a variety of factors that extend far beyond your personal claims history. While your individual record certainly matters, broader economic and industry trends play a significant role in determining what insurance costs.

Understanding what’s driving these increases can help you make informed decisions about your coverage and ensure you’re properly protected.

1. Inflation Has Increased the Cost of Everything

Just like the price of groceries, fuel, and housing has increased, insurance claims have become more expensive to settle.

When a claim occurs, insurance companies must pay for repairs, replacements, labor, materials, medical treatment, and legal expenses. As inflation drives these costs higher, insurers adjust premiums to keep pace with the rising cost of claims.

For example, repairing a vehicle today often costs significantly more than it did just a few years ago. Modern vehicles contain advanced technology, sensors, cameras, and computerized systems that make even minor repairs more expensive. The same principle applies to homes, businesses, and property repairs.

2. Rebuilding Costs Continue to Rise

Many property owners are surprised to learn how much rebuilding costs have increased in recent years.

Construction materials, labor shortages, supply chain disruptions, and increased demand have all contributed to higher rebuilding expenses. If a home, office building, church, or commercial property suffers a major loss, it will likely cost much more to rebuild today than it would have several years ago.

Insurance carriers regularly evaluate these trends and adjust property valuations to ensure coverage limits remain adequate. While this can result in higher premiums, it also helps prevent property owners from becoming underinsured when a loss occurs.

In many cases, a premium increase reflects an effort to keep coverage aligned with current replacement costs rather than simply charging more for the same protection.

3. Claims Trends, Litigation, and Weather Losses Are Impacting Everyone

Even if you have never filed a claim, industry-wide losses can affect insurance pricing.

Across the country, insurers continue to face increased claims activity from severe weather events, including hurricanes, tornadoes, hailstorms, flooding, and wind damage. These catastrophic events generate billions of dollars in losses annually.

In addition, legal settlements and lawsuit awards have grown significantly. This trend, often referred to as "social inflation," has increased liability claim costs across both personal and commercial insurance lines.

As claims become larger and more expensive, insurance companies adjust pricing to account for the increased risk exposure.

What Can You Do?

While you can’t control inflation, weather events, or industry-wide claims trends, you can ensure your coverage remains appropriate for your needs.

Rather than focusing solely on price, it’s important to understand the value and protection your policy provides. A lower premium doesn’t always mean better coverage, and cutting corners today can create significant financial exposure tomorrow.

This is where working with a local independent agent or personal risk manager can make a difference. A professional review can help identify opportunities to improve coverage, adjust deductibles, explore discounts, and ensure your policy reflects your current situation.

The Bottom Line

Insurance premiums are rising for reasons that extend far beyond individual claims. Inflation, increased rebuilding costs, severe weather losses, and rising litigation expenses are all contributing factors.

The good news? You don’t have to navigate these changes alone.

Want a quick coverage review? Let’s talk. Our Risk Advisors can help you understand your options and make sure your coverage is working as hard as you are.

Latest insights and trends

How to Build a Business Continuity Plan

Independent Contractors vs. Employees: Who Needs Insurance Coverage?

Let’s Build Your Protection Strategy